Review of “Bubbles and Crashes” by Brent Goldfarb and David A. Kirsch

Brent Goldfarb and David A. Kirsch. Bubbles and Crashes: The Boom and Bust of Technological Innovation. Stanford, CA: Stanford University Press, 2019. 247 pp. $35.00, cloth.

Financial bubbles have been a recurring phenomenon throughout the history of capitalism that have proved costly for society. According to the U.S. Bureau of Economic Analysis, the most recent financial crisis from 2007 to 2009 resulted in a real GDP loss of $650 billion. The U.S. Government Accountability Office (2013: 12) called it the “most severe economic downturn since the Great Depression of the 1930s.”

Given that financial bubbles are more the domain of finance scholars and economists, why should ASQ readers read a book on Bubbles and Crashes? Its subtitle—The Boom and Bust of Technological Innovation—is what makes the book interesting for organizational scholars. Beginning with the famous Aston studies, organizational scholars have increasingly focused on technology as a key shaper, first of individual organizations (Hage and Aiken, 1969) and later of entire populations of organizations (Tushman and Anderson, 1986). The recent interest in “disruption” typically involves a new technology that a startup develops for a niche market. Subsequently the technology is so much improved that the startup can bring it to the core market where it disrupts the leadership position of incumbent firms (Christensen, 1997). Goldfarb and Kirsch extend this literature by examining the role of technological innovation in the formation of bubbles in financial markets. They aim to identify the key causal mechanisms that increase the likelihood of the formation of a speculative bubble.

The book is divided into six chapters. After a brief introduction outlining the most important elements of their theory about the formation of speculative bubbles, chapter 1 introduces the central concepts necessary to differentiate bubbles from non-bubbles. Bubbles are those “boom and bust episodes in which investors drive up prices and get fooled” (p. 24). To determine whether there is a bubble, the authors develop a measure called “frothiness” that represents “the number of standard deviations from the predicted stock or index trend . . . where the ‘trend’ is the predicted stock price looking forward and backward seven years” (p. 35). In short, the measure indicates whether stock prices are inflated. If the frothiness is larger than 2, the stock price is a candidate for a bubble, but the authors bring to bear additional judgments to determine whether investors were fooled. Chapter 2 describes the role of uncertainty and narratives in the formation of bubbles. The authors differentiate four types of uncertainty: technological uncertainty, competitive uncertainty, business model and value chain uncertainty, and demand uncertainty. And they conceptualize narratives—which emerge in an unexpected starring role in the book––as “temporally sequenced accounts of interrelated events or actions undertaken by characters” (p. 51). Chapter 3 explains what role novices, naïfs, and biases play in the formation of bubbles. While chapters 2 and 3 constitute Goldfarb and Kirsch’s theory on the causes of speculative bubbles driven by technological innovation, chapter 4 applies their framework to a sample of technologies to test its explanatory power. In chapter 5 Goldfarb and Kirsch test the external validity of their theory by applying the framework to a different sample of more recent technologies. Chapter 6 derives policy implications from the framework and gives practical advice on how one can assess the probability of being in a bubble. The appendix provides further information on the methods, a summary of the main findings in tables, and a comprehensive list of sources used for writing the detailed histories of the technologies.

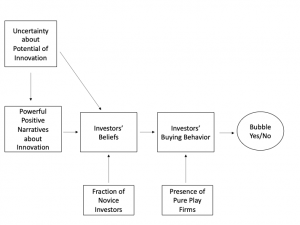

The core idea of the book is that the interaction between (1) the uncertainty pertaining to the potential of a particular technological innovation, (2) powerful positive narratives that shape investors’ beliefs about a technological innovation, (3) novice investors, and (4) so-called “pure plays” that enable investors to directly invest in a technological innovation increases the probability that bubbles form. What surprised us the most in the book is that narratives play a central role in the formation of bubbles. In the face of uncertainty, narratives serve as a means of sensemaking for novice investors to understand a new technology’s potential (Gioia and Chittipeddi, 1991). If novice investors buy into the narratives about a new technology, they are much more likely to invest in it by buying stocks of a “pure play”––a new firm that exists only to commercialize the new technology. They drive up the prices of the pure play stocks, making the formation of a bubble more likely. Tesla offers a current example of a powerful narrative that can drive the stock price to staggering heights. Tesla in 2019 sold only 368,000 cars, compared with GM selling 7.71 million. But even though GM sold 20 times as many cars as Tesla that year, in January 2020 GM’s stock was worth $50 billion and Tesla’s was worth $93 billion (Lee, 2020). The present positive Tesla narratives run like this: The car industry will have to switch in the next few years to e-vehicles to meet emissions targets. Tesla can get exciting cars out the door and now has proved that it can also mass produce these cars. Incumbent players are slow to change, and so Tesla will capture a very large market share in the coming years.

We found the book a fascinating read because it provides a role model for how the understanding of a phenomenon can be advanced through the interplay of ideas and evidence. Goldfarb and Kirsch marry historians’ sensibility with sophisticated social science methodology.

First, drawing on their historical expertise, they develop well-researched histories of all important new technologies since the mid-19th century. Although the histories were too long to print in the book, the reader can sense that the authors have carefully researched the innovations when they write about electric lighting (p. 17), the telephone (p. 26), insulin (p. 29), radio (pp. 31, 64), television (p. 33), commercial aviation (pp. 57, 116), vulcanized rubber (pp. 59, 87), the internal combustion engine (p. 67), the automatic watch (p. 105), phototype printing (p. 106), antibiotics (p. 108), hosiery (p. 108), the jet engine (p. 114), the Wankel engine (p. 118), the transistor (p. 123), oil drilling (p. 128), cortisone (p. 128), the internet (p. 134), personal computers and laptops (p. 143), liquid crystal displays (p. 146), laparoscopic surgery (p. 148), housing (p. 152), and Tesla and e-vehicles (p. 156). To make their conclusions as transparent as possible, Goldfarb and Kirsch invite readers to check and replicate their analyses, as the authors have made their data publicly available on the book’s website (https://www.sup.org/books/extra/?id=24950&i=Online%20Appendix.htm) and as they are willing to share upon request all the detailed histories. Second, the authors test-drive their framework across a large sample of technologies spanning nearly 150 years. These technologies are carefully selected across all industries to avoid a sampling bias. Third, Goldfarb and Kirsch cross-validate their framework by applying it to a second sample of more-recent technological innovations, providing further support for their framework. Fourth, to avoid confirmation bias they also test whether their framework correctly explains and predicts when a technological innovation did not result in the formation of a bubble.

Key Causal Factors Driving Bubbles in New Technology Markets

We have a minor criticism that the authors could remedy when the paperback version of the book is published. Organizational scholars—for better or worse—are used to having graphical summaries of the main theoretical arguments because they have been socialized by journals, such as the Academy of Management Review and ASQ. It would be nice to have a graphical summary of the theory in the book’s introduction to which the reader can return when the authors provide details of their ideas in later chapters. We felt a bit lost in later chapters and created the figure above for our own orientation.

No single piece of research can provide definitive support for a theory, and every methodology has its shortcomings. Goldfarb and Kirsch provide support for the theory’s external validity by examining counterfactuals of different technological innovations that did not lead to a bubble. If one wants to provide the most compelling causal evidence, it would be necessary to observe counterfactuals of the same technological innovation to demonstrate the causal effect of, for example, narratives on the formation of bubbles. This of course is not possible with historical data.

A next step in the research agenda in our view would be history-friendly simulations in which one can create exact counterfactuals in the simulations process and determine whether key causal factors hold. See, for example, the simulations by Brenner and Murmann (2016), who tested causal arguments made in a historical analysis by Murmann (2003). Another next step would be to build an experimental stock market (one can do these easily with university students), vary the availability of narratives while holding everything else constant, and observe whether bubbles form or not.

Overall, we highly recommend Bubbles and Crashes to anyone who is either interested in how technological innovations and narratives shape industry developments or who simply seeks inspiration and guidance on how to combine historical and social science methodologies.

Johann Peter Murmann and Benedikt Schuler